Managing taxes as a small business owner or independent contractor can feel overwhelming. Unlike traditional employees whose taxes are withheld from their paychecks, you’re tasked with setting aside and paying your taxes directly to the IRS yourself. That’s where estimated tax payments come in.

These quarterly payments are a way to stay ahead of your tax obligations, avoid penalties, and manage your cash flow. But don’t worry, breaking the process into steps makes calculating and paying estimated taxes much simpler than it seems.

Here’s everything you need to know about estimated taxes, why they’re important, and how to calculate them.

Don’t Get Caught Off-Guard by Estimated Taxes

Independent contractors and small business owners often dread tax season. Late or inaccurate payments can result in hefty penalties or surprise bills, a stress no one wants. The IRS collected over $1.6 billion in underpayment penalties in 2022 alone!

Estimated taxes help mitigate these issues by breaking your tax payments into four manageable installments throughout the year. By following the pay-as-you-go tax system, you can avoid end-of-year shocks while staying compliant with federal tax regulations.

What Are Estimated Taxes and Who Needs to Pay Them?

Defining Estimated Taxes

Estimated taxes are prepayments for income tax and self-employment tax. These payments ensure that individuals earning income outside a traditional W-2 structure(where taxes are automatically withheld) will still pay their share throughout the year.

If you’re self-employed, estimated taxes cover two big components of your tax responsibility:

- Income Tax

- Self-Employment Tax (Social Security and Medicare contributions)

Who Should Pay Estimated Taxes?

You’ll likely need to pay estimated taxes if you fall into one of these categories:

- Independent contractors

- Small business owners

- Individuals earning untaxed income, such as rental property income or dividends

Nerd Note: IRS rules require you to pay estimated taxes if you expect to owe $1,000 or more in taxes when you file your return.

Safe Harbor Estimated Payments

Safe harbor rules for estimated payments provide a way to avoid underpayment penalties. These rules come into play if you pay at least 90% of the current year's tax liability or100% of the prior year's tax liability (110% if your adjusted gross income was over $150,000). Meeting these thresholds ensures you won't face penalties, even if additional taxes are owed when you file your return. Safe harbor payments are particularly useful for those with fluctuating or unpredictable income, offering some stability and protection against penalties.

The 4 Steps to Calculating Estimated Taxes

Step 1 – Estimate Your Taxable Income

Your first step is to calculate how much taxable income you’ll earn during the year. Start by estimating your total income, factoring in business expenses and deductions. For example:

Meet Josh, a freelance graphic designer.

- Josh expects to earn $125,000 in net income from his business after deducting business expenses.

- He also plans to contribute $23,000 to a Solo 401(k),which reduces his taxable income.

- Additionally, Josh is eligible for the standard deduction of $15,000 (for single filers in 2025).

With these adjustments, Josh calculates his estimated taxable income to be $87,000.

Nerd Note: The standard deduction is a baseline personal tax break that reduces taxable income.

Step 2 – Calculate Self-Employment Tax

Self-employed individuals are responsible for both the employee and employer portions of Social Security and Medicare taxes, totaling 15.3%. However, only 92.35% of your net income is subject to this tax.

For Josh:

- Multiply his net income of $125,000 by 92.35%, resulting in $115,438(self-employment taxable income).

- Apply the 15.3% self-employment tax rate, equaling $17,662.

Good news, half of this tax is deductible as an adjustment to income.

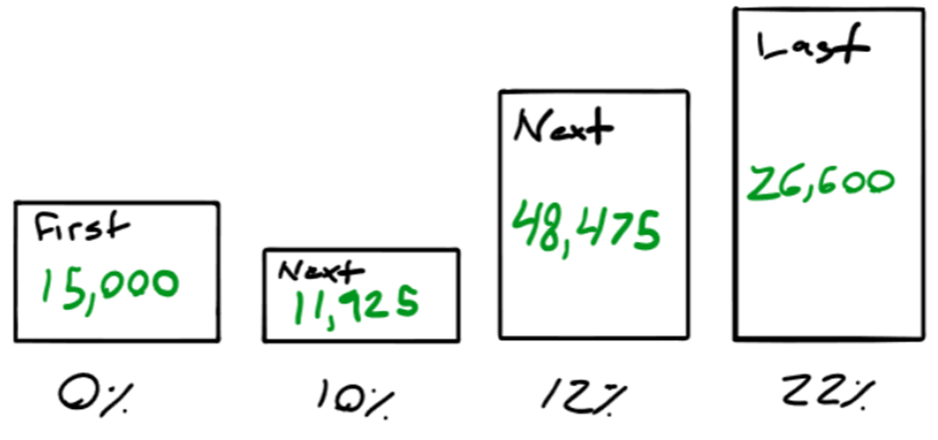

Step 3 – Calculate Your Income Tax Liability

Next, calculate your income tax liability using federal tax brackets. Josh’s taxable income of $87,000 is split across the following tax brackets (for single filers in 2025):

- 10% on the first $11,925 = $1,193

- 12% on the next $48,475 = $5,817

- 22% on the next $26,600 = $5,852

Josh’s total income tax liability is $12,862.

Nerd Note: Only the portion of income exceeding a bracket threshold is taxed at that bracket’s rate.

Step 4 – Combine and Divide for Quarterly Payments

Finally, add the self-employment tax and income tax liabilities together to calculate your total estimated taxes:

- $17,662(self-employment tax) + $12,862(income tax) = $30,524.

Divide this figure by four to determine your quarterly payments. For Josh, each quarterly payment is roughly $7,631.

If your income changes throughout the year, you can adjust your payments accordingly to avoid overpaying or underpaying.

Nerd Note: Estimated tax payments are due quarterly on April 15, June 15, September 15, and January 15of the following year.

How to Pay Your Estimated Taxes

Payment Methods

The IRS makes it easy to pay your quarterly estimated taxes through various channels:

- Online: Use the IRS Direct Pay system or the EFTPS website.

- By Check: Send payment via mail with Form 1040-ES.

- Electronic Funds Transfer : Many banks offer this service.

Keeping Track of Payments

Be sure to keep receipts or confirmation numbers for each payment you make. Accurate records will streamline tax filing at the end of the year.

Common Mistakes to Avoid

Underestimating Income

Failing to account for increased income can lead to costly underpayment penalties. Regularly revisit your income projections to ensure accuracy and ensure the safe harbor minimums have been paid in to avoid penalties.

Forgetting Additional Income Sources

Don’t overlook other income streams, such as rental property income, dividends, or your spouse’s earnings (if filing jointly).

Ignoring State Taxes

If you reside in a state that imposes income tax, remember to estimate and pay state-level taxes too.

Nerd Note: Each state has its own rules and deadlines. Don’t forget to check yours!

Stay Ahead of Tax Surprises

Estimated taxes might seem complicated at first, but breaking the process into manageable steps can make them much less intimidating. Paying quarterly ensures smooth cash flow, fewer penalties, and a better night’s sleep when tax season rolls around.

Looking for personalized help managing your taxes as a contractor or small business owner? HealthyFP is here to guide you every step of the way. Contact us today for expert advice and resources to make estimated tax payments stress-free and simple.