When it comes to building wealth, asset allocation often gets all the attention, but there's another unsung hero that can transform your portfolio's success over time. Enter asset location.

Asset location is the strategy of assigning different types of investments to specific accounts (like tax-deferred, taxable, and tax-exempt accounts) based on how they are taxed. Why does this matter? Taxes can eat into your returns, holding your portfolio back from reaching its full potential. Strategic asset location helps minimise taxes, letting your investments grow more efficiently.

Different accounts come with their own rules about how investments are taxed. Tax-deferred accounts like 401(k)s and traditional IRAs, for instance, delay your tax bill until retirement. Tax-exempt accounts, like Roth IRAs, allow tax-free growth and withdrawals. Meanwhile, taxable accounts offer no special tax advantages, but tax-efficient investments can often thrive there.

If taxes are left unchecked, they can act as a “drag” on portfolio growth. Over decades, this can add up to tens (or even hundreds) of thousands of dollars in missed potential returns.

Nerd Note: According to Morningstar, strategic asset location can boost after-tax returns by as much as 0.25% to 0.75% annually. Over the course of 30 years, that difference compounds into serious savings for investors!

The Tax Codes Investors Need to Know

Understanding Ordinary Income vs. Capital Gains

Not all investment income is taxed the same way. For example:

- Ordinary Income includes wages, rental income, or interest from bonds. These are taxed at your regular income tax rate, which can be as high as 37%!

- Capital Gains happen when you sell an investment for more than you paid. If you hold the asset for over a year, you are taxed at long-term capital gains rates, which are generally lower.

Why does this distinction matter for asset location? Investments generating ordinary income are better off in accounts with tax benefits (like traditional IRAs), while those generating capital gains thrive in tax-efficient environments (like Roth IRAs or taxable accounts).

Tax-Deferred Accounts

Examples of tax-deferred accounts include 401(k)s and traditional IRAs. These accounts shield your investments from taxation until you withdraw. This makes them ideal for:

- Bonds, which generate regular interest (taxed as ordinary income).

- REITs (Real Estate Investment Trusts), which also tend to produce taxable income.

Deferring taxes lets the investment grow without interruption, and you'll only pay taxes upon withdrawal in retirement (often at a lower tax bracket).

Taxable Accounts

Taxable accounts don’t offer upfront or withdrawal tax advantages. However, they are perfect for:

- Tax-efficient investments, like index funds and ETFs, due to their lower turnover and reduced taxable events.

- Long-term capital assets, where capital gains taxes apply (these rates are lower than ordinary income tax rates).

Tax-smart investing here can significantly reduce your annual tax bill.

Tax-Exempt Accounts (e.g., Roth IRAs)

Roth IRAs are almost magical within the realm of asset location. Contributions are made after-tax, but all growth and withdrawals are tax-free. To maximise this advantage, prioritise high-growth assets, such as stocks, in these accounts.

Consider this: A fast-growing stock held in a Roth IRA can balloon in value while remaining tax-free forever. Is there a better deal than that? (Spoiler alert: Probably not.)

How to Strategically Match Investments to Accounts

Identifying the Type of Income Your Investments Generate

Each investment generates different types of income:

- Ordinary dividends (taxed as ordinary income).

- Qualified dividends (taxed at long-term capital gains rates).

- Capital gains from appreciated assets (taxed as ordinary income if held for less than a

year, otherwise, capital gains rates). - Interest income from bonds or savings accounts (usually taxed as ordinary income).

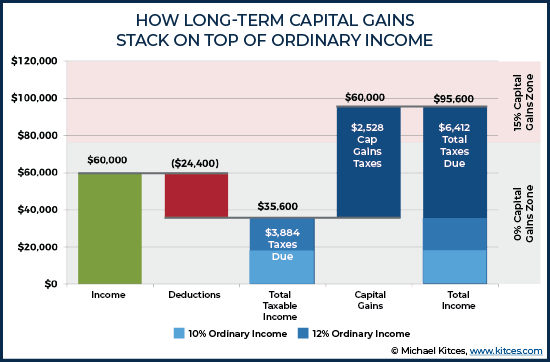

Understanding these distinctions helps you avoid overpaying Uncle Sam. The below visual from Michael Kitchen blog helps illustrate how a couple who earns $60,000 of income, taking a standard deduction would first be taxed on their ordinary income, thereafter, their capital gains income would be added on top of it.

Nerd Note: You will see that below a threshold of taxable income income ($48,350 for singles and $96,700) capital gains are taxed at a whopping 0%! This creates very exciting planning opportunities for lower income years.

Aligning Assets to the Right Accounts

Matching investments to the most tax-efficient account type isn’t as complicated as it may seem once the basics are clear. Examples include:

- Hold municipal bonds in taxable accounts, as their interest income is already tax-exempt.

- Place REITs and high-yield bonds in tax-deferred accounts to shield their ordinary taxable income.

- Choose stocks or growth-focused ETFs for tax-exempt accounts like Roth IRAs to maximise their growing potential, free from future taxes.

Balancing Risk Across Account Types

While optimising for taxes is crucial, don't forget about diversification. Ensure your portfolio remains balanced across asset classes and account types to align with your risk tolerance. A well-diversified portfolio guards against market volatility while staying tax-efficient.

Nerd Note: An oft-overlooked fact is that certain retirement accounts require Required Minimum Distributions (RMDs) after age 73. Proper asset location can help ensure you are not withdrawing heavily taxed funds unnecessarily!

Benefits of Tax Optimization in Your Portfolio

What happens when you prioritise asset location?

- Minimised Tax Drag: Fewer taxes mean more of your returns stay in your pocket.

- Enhanced Compounding: Investments grow faster when taxes does not constantly cut into gains.

- More Spending Power in Retirement: Your nest egg stretches farther for travel, hobbies, or family.

Over time, tax optimization creates a profound impact on your financial independence.

Common Mistakes to Avoid With Asset Location

Ignoring Tax Implications When Investing

Failing to consider tax impacts when choosing accounts can lead to missed opportunities for savings. Think of it this way, using a tax-inefficient strategy is like watering your garden with a leaky hose!

Prioritising Asset Allocation Without Asset Location

Asset allocation (choosing what to invest in) should work hand-in-hand with asset location (where to hold those investments). Many investors over-focus on allocation, leaving tax efficiency opportunities on the table.

Take Control of Your Wealth Through Strategic Investing

Your portfolio does not just grow because of what you invest in, it flourishes when you strategise how and where to hold those investments. With smart asset location, you can optimize your taxes, amplify your long-term returns, and pave the way for financial flexibility in retirement.

Are you ready to align your investments with your goals and values? Contact a HealthyFP financial planner today for personalised guidance, and take the first step toward maximising your portfolio’s potential.