Taxes are one of life’s unavoidable certainties, but understanding how they work can feel overwhelming, especially when you're juggling income, investments, and financial planning. Whether you’re a small business owner, an individual investor, or part of the workforce, gaining insight into how taxes are calculated can save you time, stress, and, most importantly, money.

From the nuances of tax brackets to the taxation of investment accounts, this guide will break it all down for you in an easy-to-follow way. Let’s demystify taxes so you can approach tax season (and year-round tax planning) with confidence.

Avoid Common Misconceptions About Taxes

Many people fear tax season, believing it’s more confusing than it needs to be. Have you heard someone say, “If I earn more, I’ll pay that higher tax rate on everything I make”? Thankfully, that’s not how it works.

Taxes in the U.S. are tiered or "layered," like filling buckets. Each portion of your income falls into a specific "tax bracket," where it’s taxed at progressively higher rates beyond certain thresholds. This approach creates fairness while helping you retain more of the money you earn.

Understanding how ordinary income, capital gains, and investment accounts are taxed can help ease your anxiety and spark smarter tax strategies.

How Is Ordinary Income Taxed?

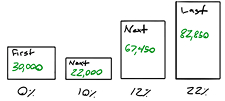

Breaking Down Tax Brackets

The U.S. tax system is progressive, meaning income is taxed in portions at different rates. Think of taxes as “filling buckets”:

- First bucket of income is taxed at the lowest rate (e.g., 10%).

- Second bucket is taxed at a slightly higher rate (12%).

Each new bucket (or tax bracket) gets taxed at incrementally higher rates.

Marginal Tax Rate vs. Effective Tax Rate

- Marginal Tax Rate is the rate you pay on your next incremental dollar of income.

- Effective Tax Rate is the average percentage you pay in taxes, calculated as your total tax divided by your total taxable income. This is always lower than your marginal rate.

Example: If you’re married and earn $200,000 in 2025, the first $30,000 at least is deducted using the standard deduction, from there the remaining income fills up the following tax brackets. In this case, every additional dollar is taxed at 22% marginal rate, but their effective rate is 16%!

How Are Bonuses Taxed?

Bonuses often come with confusion. Many think they’re “taxed more,” when in reality, they’re just taxed at 22% of income up to $1M and 37% in excess of $1M. The misunderstanding arises from the differed rate applied to bonuses versus typical pay cycles, which only impacts your short-term paycheck, not your overall tax liability.

Key Takeaways

- Income is taxed in layers, using progressively higher percentages.

- Marginal Tax Rate applies only to new dollars you earn.

- Bonuses aren’t taxed extra, they’re just withheld differently!

Understanding Taxes on Capital Gains

What Are Capital Gains?

Capital gains are the profits made from selling investments outside of retirement accounts or property. The tax rate depends on how long you held the asset:

- Short-term gains (assets held less than 1 year): Taxed at ordinary income rates.

- Long-term gains (assets held more than 1 year): Earn preferential tax rates of 0%, 15%, or 20%, depending on your income.

Examples of Short-Term vs. Long-Term Gains

Here’s a quick breakdown with numbers to visualize the difference:

- Short-term gain:

- Married couple earning $250,000 sells an investment bought for $10,000 at $20,000 after 6 months.

- Total gain = $10,000, taxed at their 24% marginal rate.

- Tax due = $2,400.

- Long-term gain

- If the same couple held the $10,000 investment for 18 months, the gain would qualify for the preferential long-term capital gains rate (likely 15%).

- Tax due = $1,500 saving $900.

Nerd Note: Long-term capital gains don’t just apply to stocks, they can include property sales too! By holding investments longer, you can unlock substantial tax savings.

What About the Net Investment Income Tax?

High earners face an additional 3.8% tax known as the Net Investment Income Tax (NIIT). This applies to individuals earning more than $200k or married couples earning more than $250k.

Key Takeaways

- Hold investments for more than a year to access lower long-term capital gains tax rates.

- Be mindful of the NIIT if your income crosses the high-earner threshold.

Tax Treatment of Investment Accounts

Roth, Traditional, and Taxable Accounts

- Roth Accounts: Taxes paid up front (no different than if it landed in your bank account in year 1); withdrawals during retirement are tax-free.

- Traditional Accounts (e.g., 401(k), IRA): Contributions are untaxed initially (deducted in year of contribution); withdrawals on contributions and gains are taxed as ordinary income during retirement.

- Taxable Accounts: Contributions are made with after-tax dollars. Capital gains are taxed when realized, offering flexibility and growth potential.

Which Account Is Best?

Choosing the right account depends on your tax bracket and goals.

- Higher earners often favor tax-deferred Traditional accounts for current tax relief.

- Younger, lower-income earners may benefit more from Roth accounts due to their future tax-free withdrawals.

Pro Tip: Diversify across Roth, Traditional, and Taxable accounts to allow flexible, tax-efficient withdrawals in retirement.

Key Takeaways

- Roth = Tax-free growth for retirement.

- Traditional = Defers taxes, ideal for high-income earners toda

- Taxable = Great for long-term growth and early withdrawals taxed as capital gains.

Why Understanding Taxes Matters

Taxes touch every financial decision you make, from your paycheck to selling an investment to planning your next big move. Understanding tax brackets, capital gains, and account options enables smarter choices that lower your tax bill, grow your wealth, and secure your financial future.

At HealthyFP, we simplify the complexities of taxes and investments. Whether you’re planning for next year or fine-tuning a long-term plan, our expert team is here to help.

Ready to take control of your taxes? Schedule a consultation with HealthyFP today and start making tax-smart decisions for a more confident tomorrow.