Managing an inherited IRA can feel overwhelming, especially given the complex rules and significant tax consequences. Imagine this scenario: You’ve just inherited a loved one’s IRA, a financial blessing wrapped in layers of IRS regulations. Without proper planning, this new resource could result in unnecessary tax penalties, costing you tens of thousands of dollars. However, with the right strategy, you can reduce your tax liability and make the most of this inheritance.

This guide will walk you through what an inherited IRA is, common mistakes to avoid, and strategies to minimize your tax burden, all to help ensure your financial well-being.

What Is an Inherited IRA and Why It Matters

When you inherit an IRA, it’s not just another account, it comes with its own set of rules and tax implications that you must manage carefully.

What Is an Inherited IRA?

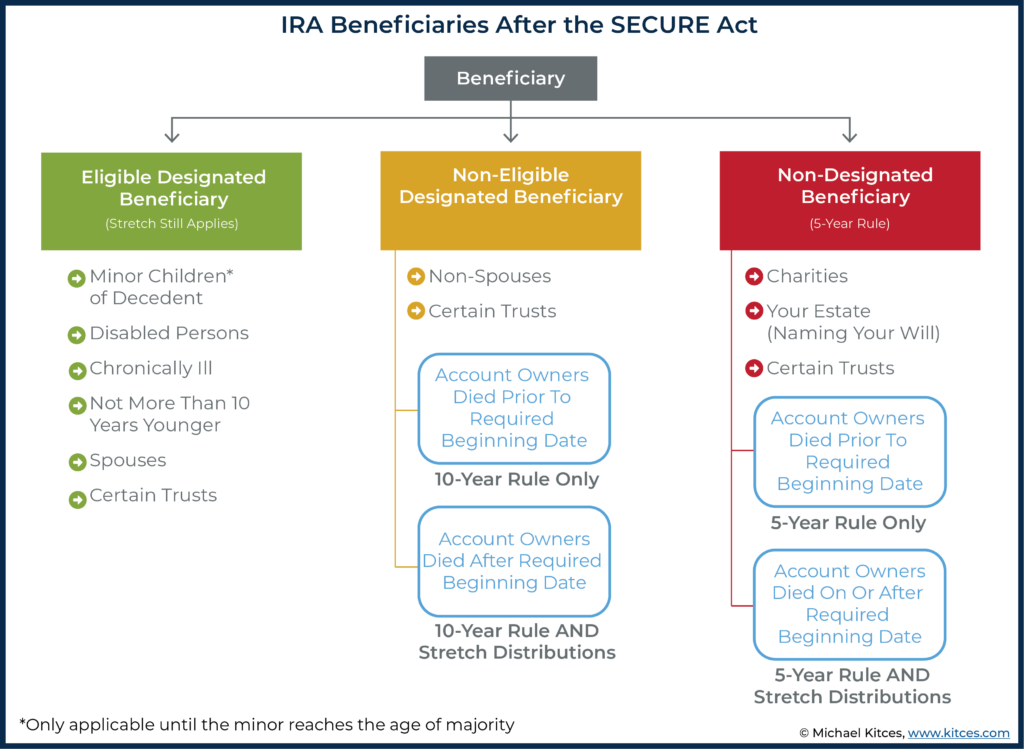

An inherited IRA is an individual retirement account that you inherit from someone who has passed away. If you’re not an "eligible designated beneficiary" (most commonly spouse, minor or within 10 years), recent changes to the rules, following the SECURE Act in 2020, require that you distribute the full balance of the inherited IRA within 10 years after receiving it.

This 10-year rule can feel like a ticking clock when it comes to managing distributions, especially since withdrawing the full amount in one year can be incredibly costly in taxes.

Below is a visual from Michael Kitces to help understand what rules apply to different beneficiaries and note that those who inherited from someone already taking required distributions are required to continue to take distributions each year in most cases rather than needing to be fully withdrawn at the end of the state timeline.

Nerd Note: Did you know that failing to properly plan the distribution of an inherited IRA could lead to tax bills totaling over 32% of your inheritance? That’s money going straight to the IRS instead of staying in your pocket!

Eligible Designated beneficiaries, on the other hand, have more flexible options, like rolling the inherited IRA into their own existing retirement account.

Common Missteps When Managing an Inherited IRA

Managing an inherited IRA requires strategy. Here are three common mistakes that can result in massive tax penalties.

Taking the Full Lump Sum

Cashing out the entire inherited IRA at once may seem like the simplest solution, but it can push you into a higher tax bracket. This might trigger higher federal income taxes, Medicare premium hikes, and even state income taxes.

Example: Bob and Sue inherited a $1,000,000 IRA. If they withdrew the entire amount in one year to purchase a home, their additional income landed them in a higher tax bracket, leading to an eye-watering $325,000 in taxes!

Not Setting Up an "Inherited IRA" Properly

If you don’t roll the inherited funds into a properly titled “inherited IRA,” you may lose critical tax benefits. Unlike standard IRAs, inherited IRAs require special handling to ensure compliance with IRS rules.

Procrastinating Until the 10-Year Deadline

Waiting too long to start taking distributions can lead to large mandatory withdrawals in the final years, creating a massive tax burden. Proactive planning allows you to spread distributions over the entire 10 years, reducing the overall tax impact.

Proactive Steps for Managing an Inherited IRA

Thankfully, there are strategies you can implement to minimize taxes and maximize the value of your inherited IRA.

Spread Distributions Over 10 Years

Rather than wait until the 10th year, consider spreading distributions evenly over the decade, or better yet in years you are likely to have lower income to help lower your lifetime tax bill. This approach helps you stay in a lower tax bracket and avoid costly surprises.

Example: If Bob and Sue had spread their $1,000,000 inheritance across 10 years, their total tax bill could have been just $240,000 instead of $325,000, saving them $85,000!

Incorporate Tax Planning Early

Consult with an accountant or financial advisor immediately after inheriting an IRA. Early guidance can help outline a strategic plan that reduces your tax liability while aligning distributions with your overall financial goals.

Evaluate Your Current Financial Picture

Take a look at your existing income, investments, and expenses (like health care). For example, higher reported income could increase your Medicare premiums. A comprehensive understanding of your financial landscape ensures distributions align with your larger goals.

How to Set Up an Effective Plan

Here’s how you can manage your inherited IRA with efficiency and clarity.

Find the Right Team

Partner with a tax preparer or financial planner who is familiar with inherited IRAs. These experts can help you craft a "master plan" that ensures compliance with IRS rules and limits taxes.

Account for Legislative Changes

Tax laws around inherited IRAs evolve. For example, the SECURE Act replaced the long-standing “stretch IRA” option with the 10-year rule. Stay informed about changes to maximize your benefits.

Leave a Legacy for Future Generations

After setting up your inherited IRA, consider how you can prepare your own beneficiaries for future inheritance. Clear communication about the rules and a transparent financial plan can ensure that your legacy is protected.

Nerd Note: The SECURE Act of 2020 increased federal tax revenue by introducing the 10-year rule for inherited IRAs while ending the "stretch IRA" approach. The result? More taxes due in a shorter period, and more pressure on beneficiaries. Avoid these pitfalls with proactive planning.

Key Takeaways for Long-Term Financial Health

Successfully managing an inherited IRA is about understanding the rules, avoiding common mistakes, and considering proactive strategies.

Here’s what you need to remember:

- Use the 10-year rule to your advantage by spreading distributions evenly.

- Collaborate with a tax professional or financial advisor early for expert guidance.

- Regularly review your financial picture to mitigate unintended consequences like higher taxes or Medicare penalties.

Don’t leave your inheritance management to chance. The HealthyFP team is here to guide you through every step of the process.