Picture this: You’ve just come into a financial windfall. Maybe it’s a work bonus, an inheritance, or years of diligent saving. You’re holding $500,000 in cash and know you need to invest it, but here’s where the anxiety sets in. What if you invest it all at the wrong time? What if the market takes a sudden dip the day after? Or, on the other hand, what if you miss out on potential growth by waiting too long?

You’re not alone in this dilemma. The decision of how to invest, a lump sum all at once or incrementally over time, is one that leaves many investors feeling torn. But don’t worry. We’re here to unpack the pros, cons, and the key considerations of both strategies so you can make an informed choice.

What Is Lump Sum Investing?

Lump-sum investing is when you invest your entire available amount into the market all at once. This approach takes advantage of the market’s long-term upward trend, but it’s not without its challenges.

Pros of Lump Sum Investing:

- Higher Potential Returns – Historically, markets tend to rise over time. By investing everything immediately, you’re exposed to the market’s growth sooner.

- Simplified Decision-Making – It’s a one-and-done approach, no need to track recurring contributions.

- Immediate Market Participation – Your money starts working for you right away.

Cons of Lump Sum Investing:

- Market Timing Risk – If the market dips soon after your investment, the impact on your portfolio will be immediate.

- High Volatility – You’ll have to stomach the rollercoaster of market ups and downs.

- Psychological Stress – Putting everything in at once can feel like gambling, especially for risk-averse investors.

What Is Dollar-Cost Averaging (DCA)?

Dollar-cost averaging is the practice of investing a set amount at regular intervals, regardless of market conditions. Essentially, it spreads your investments out over time.

Pros of DCA:

- Reduces Timing Risk – By averaging out your investments, you're less likely to catch the market at a peak.

- Mitigates Volatility Effects – Small, consistent investments smooth out the emotional impact of market swings.

- Psychological Comfort – Perfect for those who prefer a more cautious approach.

Cons of DCA:

- Potentially Lower Returns – Research shows DCA often yields lesser returns compared to lump sum.

- Discipline Required – You have to stick to your plan, even when markets are fluctuating or headlines sound scary.

Nerd Note: Think of DCA like buying concert tickets over time. Some months you’ll snag cheap tickets; other months might cost more. But, in the end, you’ve got seats to all the best shows (or market gains).

A Real-Life Example

Imagine an investor named Sarah. She has $500,000 to invest. Here’s how lump-sum investing compares to dollar-cost averaging for her:

- If Sarah invests $500,000 immediately: Assuming an 8% average return, her portfolio might grow to $540,000 by the end of the year.

- If Sarah uses DCA, investing $41,667 monthly over 12 months: With the same return rate, but factoring in market fluctuations, her portfolio could grow to $530,000.

The difference? Lump-sum investing outpaces DCA, but only slightly. And remember, his scenario assumes a steadily rising market. During volatile periods, the gap could be different.

Factors to Consider When Choosing a Strategy

Every investor is different, so the “right” approach depends on your situation. Here are key factors to weigh:

1. Risk Tolerance

- If you can handle market swings without losing sleep, lump-sum investing might be your best bet.

- If you’re cautious or prone to panic-selling, DCA can help reduce stress.

2. Time Horizon

- The longer your time horizon, the less your entry point matters, markets tend to smooth out over decades.

- If your horizon is shorter, DCA may reduce the risk of catching a market downturn.

3. Current Market Conditions

- Confident in a steadily rising market? Lump sum can capitalize on that growth.

- Facing uncertainty or volatility? DCA spreads out risks more evenly.

4. Behavioral Biases

- Are you quick to hit the sell button during a dip? Opt for DCA.

- Can you stay patient and avoid knee-jerk reactions? Lump sum could work.

Nerd Note: Behavior plays as critical a role in investing as strategy selection. Studies show that consistency, staying invested, regardless of method, is often the strongest predictor of long-term wealth.

What Does the Research Say?

Data supports lump-sum investing as the statistically superior choice 66% to 75% of the time. However, it's essential to note that long-term market trends provide this edge. If you’re investing during a downturn or recessionary period, DCA could prove the better choice by reducing volatility shock.

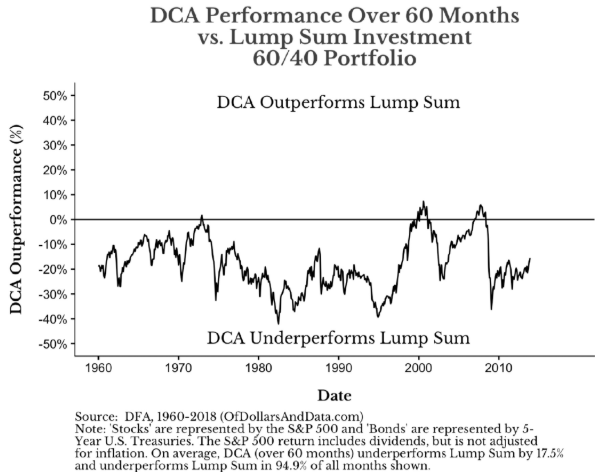

For those invested in a moderate risk portfolio, the below chart from the Ofdollarsanddata blog depicts that nearly 95% of the time dating back to 1960, the DCA approach underperforms an average of 17.5%:

Nerd Note: A Vanguard study found that lump-sum investing outperformed dollar-cost averaging (DCA) about 66% of the time. Even better, it typically yielded 1.5% to 2.4% higher returns on average. That's solid food for thought!

Expert Wisdom

Morgan Housel once said, “Average returns sustained for an above-average period of time lead to extraordinary returns.” Whether you choose lump sum or DCA, staying consistent and invested over decades is what truly counts.

Pro Tip: For those that determine the DCA approach is right for them, this should be implemented over no more than a 6 month period to have less cash on the sideline sitting idle.

A Balanced Perspective for Investors

Ultimately, lump sum and DCA aren’t rival approaches, they’re just tools in your investment belt. The choice between them often comes down to your personality, financial situation, and goals.

Here’s a comforting thought: what matters most isn't how you start, but that you start at all. Even the “wrong” strategy beats sitting on the sidelines, paralyzed by indecision.

Nerd Note: The biggest investing mistake? Waiting for the perfect entry point. Historically, time in the market beats trying to time the market.

Take Action Today

Now that you know the pros, cons, and key considerations of each approach, take a moment to reflect on what feels right for you. Investing isn't about perfection; it's about creating a plan and sticking to it.

Need help deciding? The HealthyInsights team is here to guide you. Book a consultation today and start your investing journey with confidence.