Managing your retirement accounts and planning your legacy just got more complex, and potentially more flexible. The SECURE Act introduced significant changes to Required Minimum Distribution (RMD) rules, shifting the landscape for retirees and high-net-worth individuals alike. If retirement savings and wealth transfer are important to you, it’s crucial to know how these updates affect timelines, taxes, and beneficiaries.

This blog explores the RMD rules, their impact on tax planning, and strategies to protect your assets and heirs.

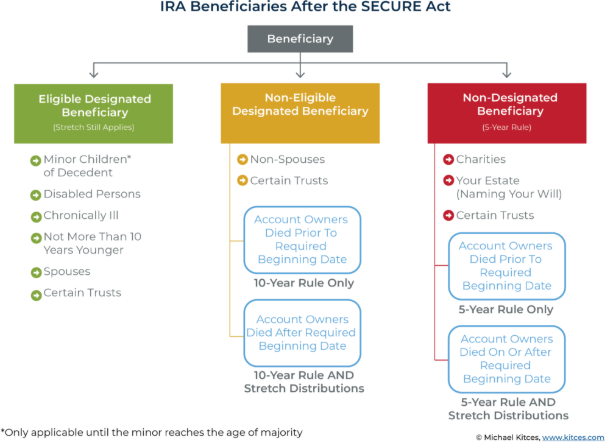

The Changing Landscape of RMDs Post-SECURE Act

The SECURE Act has brought sweeping reforms to RMD regulations. RMD’s remain required at 72 for those born in 1950 or earlier, have been pushed to age 73 for those born in 1951-1959, and those born in 1960 or beyond need to begin distributions at 75. These distributions begin at roughly 4% of the balance and increases over time.

Previously, most beneficiaries could stretch distributions using their own life expectancy, helping spread tax payments over time. However, the new rules categorize beneficiaries into Eligible Designated Beneficiaries (EDBs) and Non-Eligible Designated Beneficiaries (NEDBs), with different timelines and requirements for each.

Understanding how these categories apply to you and your heirs is essential for crafting a tax-efficient and compliant financial strategy.

Why RMD Planning Matters

For retirees and high-net-worth individuals, RMDs are more than annual withdrawals—they are a crucial element of tax planning. Any changes to these rules can significantly alter your wealth management & legacy strategy.

Nerd Note: Did you know the penalty for missing an RMD used to be a crushing 50%? Although it’s been reduced to 25%, that's still a hefty price to pay for non-compliance.

The Updated RMD Rules At a Glance

Before SECURE Act vs. After SECURE Act

Pre-SECURE Act: Beneficiaries were allowed to stretch distributions over their lifetimes, providing flexibility and minimizing annual tax burdens.

Post-SECURE Act: Most beneficiaries must now adhere to a 10-year distribution rule, requiring the depletion of inherited accounts within ten years of the original owner’s death.

Below is a helpful visual of who is considered eligible, non-eligible, and the respective distribution requirements associated with each:

This overhaul has made tax planning for inherited IRAs significantly more challenging, but knowing the details allows for better preparation.

The 10-Year Rule Explained

Under the SECURE Act, the 10-year rule applies differently based on whether the original account owner passed before or after their RMD start date.

- Pre-RMD Start Date: Beneficiaries can deplete the account anytime within 10 years without immediate RMD obligations.

- Post-RMD Start Date: Beneficiaries may need to calculate and satisfy "hypothetical" RMDs for years when distributions weren’t taken.

Key Takeaway: Surviving spouses (as well as all EDB’s) enjoy the most flexibility, including options to roll over accounts into their own or apply the 10-year rule.

Nerd Note: If you’re a spouse opting for the 10-year rule, consult a tax planner to avoid surprises with hypothetical RMD calculations.

How the New Rules Impact Tax Planning

Timed Distributions to Minimize Taxes

The timing of your RMDs matters more than ever. By spreading distributions over several years, when possible, you can avoid income spikes that push you into a higher tax bracket.

The Lost Roth Conversion Strategy

One major downside of the SECURE Act? It eliminated a helpful tax planning loophole that allowed you to perform Roth IRA conversions before satisfying RMDs for the year. Now, all distributions count towards your RMD requirement first.

Pro Tip: By starting tax planning early in the year, you may still be able to balance RMD fulfillment with long-term Roth conversion strategies.

Nerd Note: Keep in mind, Roth IRAs have no RMD requirements while you’re alive, making them a great tool for tax diversification.

Protecting Your Heirs

The new RMD rules don’t just impact your taxes, they also change the way your heirs can inherit and use your retirement savings.

Benefits for Eligible Beneficiaries

Eligible Designated Beneficiaries (e.g., spouses or minor children) have more favorable distribution options, but there are limitations. For example, minor children lose their status as EDBs when they turn 21, at which point the 10-year rule kicks in.

Employer Plans vs. IRAs

If your retirement savings are held in an employer-sponsored plan, rollover rules can be restrictive. Rolling assets into an IRA offers your beneficiaries more control and flexibility over distributions.

Missed RMD Penalties

While missed RMD penalties have been reduced from 50% to 25%, you can reduce this penalty further to 10% if the mistake is corrected promptly. For inheritors of accounts during 2021–2024, the IRS waived annual RMD requirements to provide some transition time.

Key Strategies for Adapting to RMD Changes

1. Regularly Review Your Retirement Plan

RMD rules tie closely to annual income and tax brackets, so it’s more critical than ever to revisit and adjust your strategy regularly.

2. Utilize Charitable Gifting Strategies

Qualified Charitable Distributions (QCDs) allow you to meet RMD requirements while supporting a cause you care about, and they’re tax-efficient to boot. If you intend to give to charity or a religious institution, consider nominating them as beneficiaries of the IRA, leaving more assets elsewhere for your heirs that they do not need to pay tax.

3. Empower Your Heirs

Educate your heirs on applicable RMD rules to help them avoid missed deadlines or penalties. Clear communication can prevent costly misunderstandings.

4. Consult Financial Professionals

These new rules are complex. A trusted financial advisor can provide custom strategies to ensure compliance and optimize plans for taxes and wealth transfer.

Nerd Note: Did you know financial gifts often appreciate in value when given sooner rather than later? This makes gifting a win-win strategy in RMD planning.

Plan for Your Future, Protect Your Legacy

The revised RMD rules may seem daunting, but they present new opportunities for those who plan carefully. By staying informed, you can minimize taxes, maximize returns, and ensure a smoother wealth transfer for future generations.

Don’t leave your retirement and legacy to chance. Schedule a consultation with HealthyFP today. Our experts can tailor a strategy suited to your unique needs, keeping you compliant and focused on your financial goals.