Your 401(k), one of the most powerful tools for saving, could either pave the way for a financially secure retirement or lead to missed opportunities. Too often, terms like "vesting" and "mutual funds" create a barrier for young professionals and employees who are just beginning their financial journeys. But fear not, understanding and optimizing your 401(k) isn’t as complicated as it seems.

Below, we’ll guide you through smart strategies to maximize your 401(k) benefit, prepare for the future, and build confidence in your financial decisions.

Why a Thoughtful 401(k) Strategy Matters

The Power of Compound Growth

One of the most exciting benefits of your 401(k) is the ability to harness the power of compound interest. The earlier you contribute, the longer your investments have to grow exponentially. Think of your contributions as seeds, the sooner you plant, the larger your harvest will be.

Benefits of Employer Matching

Employer matching is essentially free money, and who wouldn’t want that? Many companies will match your contributions up to a certain percentage, essentially doubling your investment. If you’re contributing less than the match, you’re missing out on an instant 100% return on that part of your investment.

Key Steps to Maximizing Your 401(k)

Step 1: Understand Your Plan

Start by reading your company’s 401(k) plan document. This dense but all-important resource outlines essential details of your plan, such as employer match percentages, vesting schedules (when your employer’s contributions become yours), and available investment options. If you don’t have a copy of your plan, your HR department will be happy to provide it, it should also be available in the documents section of your login.

Step 2: Choose Roth vs. Traditional Contributions

Understanding the difference between Roth and traditional 401(k) contributions is critical.

- Traditional 401(k): Contributions are made pre-tax but taxed along with the earnings upon withdrawal during retirement.

- Roth 401(k): Contributions are made post-tax, allowing your money to grow and be withdrawn tax-free.

Nerd Note: If you’re in the early stages of your career, a Roth 401(k) might be better, your income (and tax bracket) will likely increase over time, so paying taxes now could save you more later.

Pro Tip: Within the plan document, you may find that your plan allows for “after-tax” contributions with “in-plan conversions”, if this is the case, you are eligible to contribute up to another $46,500 to your Roth account via the “Mega-Backdoor Roth” strategy. For more details, check out our post on this way to supercharge your savings.

Step 3: Diversify Your Investments

Diversification is the golden rule of smart investing. Within your plan you will have the option to elect a “Target Date Fund”, which is managed in a way that gets more conservative as you reach your retirement date. While this is the standard and easy button for your allocations, they often become more conservative and have more allocation to international stocks than you may be aware of.

The more nuanced approach, that you may consider if you would like to dedicate time to research or working with an advisor would be to select the individual funds to customize your investments. Rather than relying on single stocks or high-fee options, the below categories will be mainstays to consider:

- Large-cap stocks: Stable, well-established U.S. companies valued at over $10 billion.

- Mid-cap stocks: Companies in the U.S. valued between $2-10 billion

- Small-cap stocks: Higher risk, higher reward U.S. investments in smaller companies valued under $2 billion.

- Developed International: Developed country stocks (such as the EU) beyond U.S. borders for added resilience.

- Emerging Markets: Further exposure to countries that are not developed for broader exposure.

- Core Bond Fund: A basket of bonds usually tracking a bond index to manage risk.

- Stable Value Fund: Typically offered by insurance companies, some offer favorable rates with minimal risk.

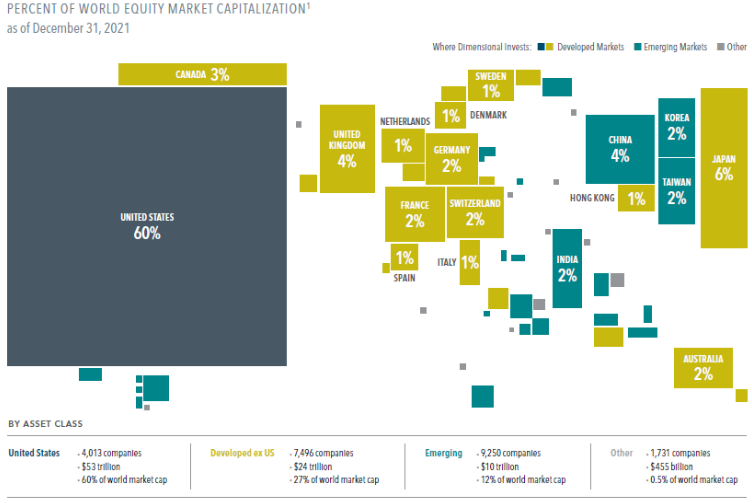

Determining how to allocate your portfolio requires a detailed look into your personal finances. If in doubt, default to the Target Date fund before further research. Below is a helpful guide of how the rest of the world allocates their finances based on the value within different geographies:

Nerd Note: While hard to believe, Russia, India, and China are all considered “emerging” market investments, so your exposure will be limited if you do not allocate to a fund there.

Step 4: Keep Fees in Check

High fees can dramatically reduce your returns over time. When reviewing mutual fund options, pay attention to expense ratios and management fees. Opt for low-cost funds to better control your experience.

Nerd Note: Mutual funds with lower fees are 3x more likely to outperform higher-cost funds over the long term, according to Morningstar.

Step 5: Review Your Beneficiaries

Life changes, your 401(k) should, too. Marriage, divorce, children - any major life event warrants reviewing and updating your beneficiary form to ensure your savings go to the right person.

Nerd Note: If you prematurely leave this earth, and an ex is listed as your beneficiary, but your Will says you want your spouse to receive everything, your ex is legally entitled to your 401(k). Be sure to have everything reviewed pending major life changes.

Step 6: Revisit Your Plan Annually

Your financial goals and circumstances evolve, so your 401(k) strategy should as well. Assess your contributions and investments yearly, and consider shifting to more conservative options as you near retirement to protect your nest egg.

Avoiding Common 401(k) Mistakes

Not Contributing Enough

If your employer matches contributions, aim to contribute at least enough to get the full match. Anything less is leaving money on the table.

Cashing Out Early

Withdrawing funds early has steep consequences, including taxes, penalties, and stunted growth potential. Avoid tapping into your 401(k) unless it’s an absolute last resort. Many 401(k)’s allow for loans, which can be paid back with future paychecks when in a pinch, and will alleviate tax to pay AND early withdrawal penalties.

Panicking During Market Downturns

Markets fluctuate, it’s part of the process. Don’t make emotional decisions during downturns. Stick to your plan and focus on long-term growth.

Smart Investing Starts Today

Your 401(k) isn’t just a workplace benefit, it’s your gateway to a secure and comfortable retirement. By leveraging employer matching, diversifying your investments, and keeping an eye on fees, you can ensure your savings work as hard as you do.

Still feeling overwhelmed? At HealthyFP, we believe everyone deserves financial clarity and are here to help you refine your strategy and make smarter financial choices.